A Step-by-Step Guide to Filling the CFPB Form 1003 (Uniform Residential Loan Application)

Whether you see yourself as a future homeowner or an emerging investor, your first mortgage is your entry point into leverage, structure, and long-term wealth building. This is your mindset, when you finally decide, and commit to yourself, that you want to own several real estate properties, in the future—in the near future. Stepping into real estate for the first time, with a strong foothold, understanding that you are positioning yourself within a financial system that has been shaping ownership for generations, whether you just want to own a home for yourself, co-own with others or dive into the business side of it. How exciting! But first we must prepare to feel comfortable filling-in Form 1003.

Approach this time with a clear objective, and turn the act of signing this form as your blueprint for ownership. Treat this like a framework of your wealth strategy, more than an application.

Because once you understand how to organize your financial life into this type of structure, the next application would be a breeze—you’re stepping into the power of Ownership. Allow yourself to dream bigger, it starts with the first one, then the next, next thing you know you have 5 or more properties on your portfolio. For many, the process feels overwhelming: credit, income, down payment, paperwork. You might be thinking, “I don’t know where to begin.” This is where I come in to guide you to have the best 1003 experience!

Experience Form 1003

At its core, the path to approval follows a clear framework—one that institutions like Fannie Mae and Freddie Mac have standardized over time. Once you feel comfortable, the process becomes less anxious and more about organizing and expanding your potential. Right? Yes.

Mindset shift

This Holistic approach focuses on your mindset. Your first goal is simple: secure a mortgage and purchase your first property. But there’s a deeper objective behind it. It is Ownership Empowerment. Understanding the structure well enough that your first purchase becomes your foundation, and your vision for your success is that this is not a one-time event.

The Official Document

You’ve got to feel love first ❤️. “Form 1003 is the holy grail of mortgage documents.” This is the form that the lenders will first see about you, and they will use it to understand your financial picture, evaluate risk, and determine your eligibility for a mortgage, along with other supporting documents you’re required to attach to complete your mortgage application. So, fill it out with confidence and give the Lender the full picture, making you a strong candidate for a mortgage loan approval. Call me or email me directly if you have any questions. This guide breaks down the form, step by step so you can approach it with clarity and confidence.

Disclaimer: The Form 1003 is maintained and periodically updated by entities such as the Consumer Financial Protection Bureau, Fannie Mae, and Freddie Mac. This blog is for educational purposes only. Fields, formats, and requirements may change over time. Always refer to the most current version provided by your lender or official sources.

These steps can be on ink or e-document.

When completing the Form 1003 (Uniform Residential Loan Application), the information may be provided by filling out the form with ink, quill—cool but not recommended. It may give your application a ‘historic feel’, but between the ink spills, feather trimming, and waiting for the ink to dry, your loan process might take longer. As your mortgage loan originator, I will accept an application in any format as long as its legibly written, complete, properly communicated, signed, and dated.

But, I highly recommend, completing it electronically through a digital document platform. Regardless of the format, the purpose remains the same: to accurately capture your financial information, personal details and loan request.

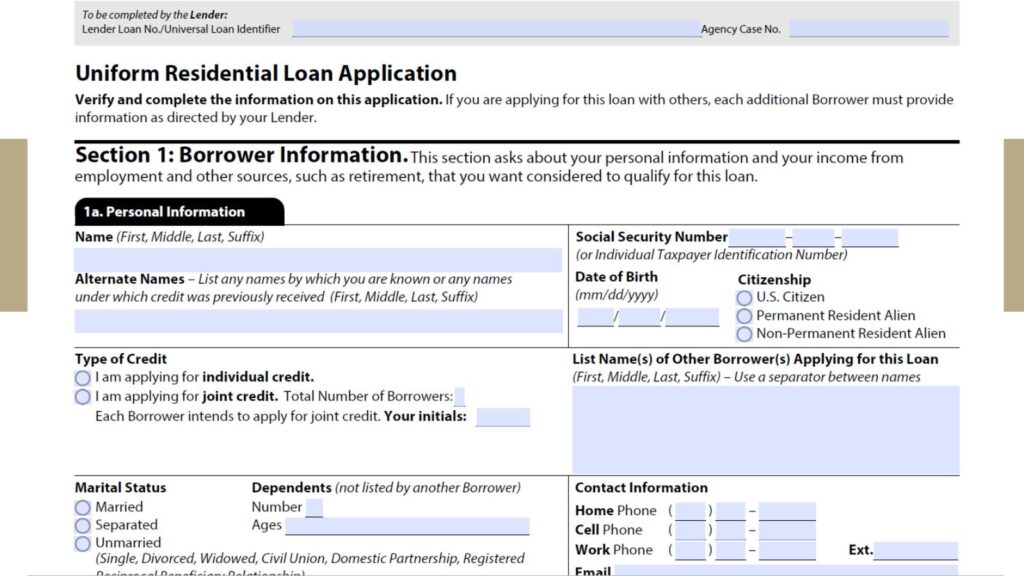

As in all living things, we have identifiable information. The first section on Form 1003 is your personal information.

1. Personal Information

This section establishes your identity. You’ll provide the following:

- Full legal name (no nicknames)

- Social Security Number

- Date of birth

- Citizenship status

- Marital status

- Number of dependents.

How exciting and easy! This is your financial identity being formalized on paper or e-document. Hang in there—there’s no need to rush through the process. Taking your time ensures the information is accurate and complete. However, if you’re working toward a specific rate lock or time-sensitive deadline, you can absolutely complete this form in less than an hour.

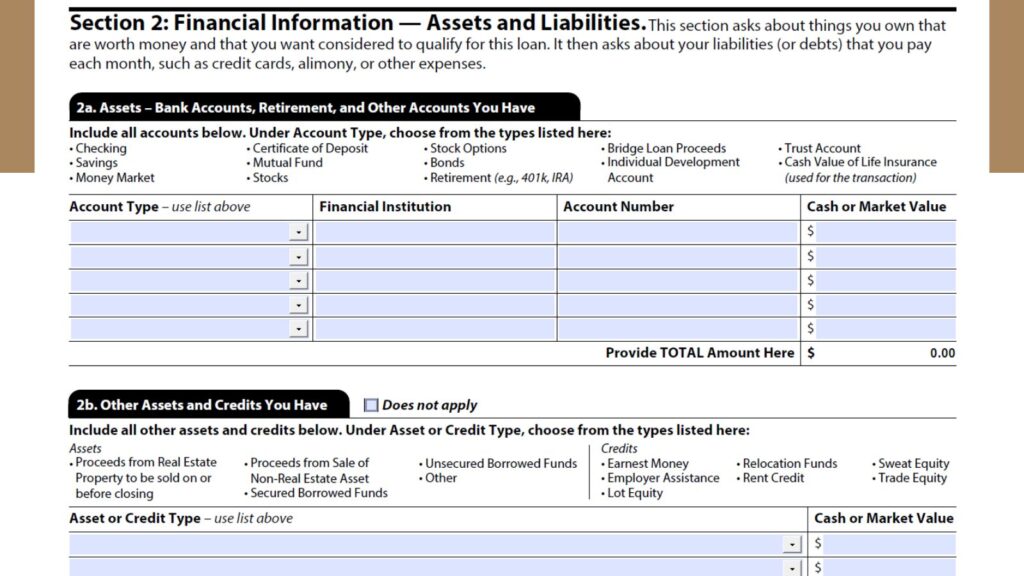

2. Financial Information

The next step is the Financial Information. The Assets & Liabilities section of your life). Here, you just have to disclose what you own and what you owe.

Assets means what you currently own.

- Bank accounts (checking, savings)

- Retirement accounts (401k, IRA)

- Stocks, bonds, crypto (if applicable)

- Any Real estate that you already own

Liabilities are what you owe

- Credit cards

- Auto loans

- Student loans

- Personal loans, and other type of loan

- Existing mortgages

The Financial Algorithm

What Lenders don’t openly tell you is they’re evaluating your behavior with money, not just your total debt or credit. There are metrics involved on how lenders evaluate your financial behavior. A system called Automated Underwriting System or AUS for short. Instead of a file being judged solely by a human underwriter, your application—built from Form 1003—is run through algorithmic models developed by institutions like Fannie Mae (Desktop Underwriter) and Freddie Mac (Loan Product Advisor).

At its core, AUS evaluates patterns: income stability, credit behavior, asset strength, and risk layering. The algorithm can be friendly, “does this person qualify?” or not too friendly. It asks, “How predictable is this borrower’s financial behavior over time?”

The result is NOT a simple yes or no—it’s a recommendation:

- Approve/Eligible

- Refer (manual review)

- Caution (higher risk)

AUS rewards consistency and structure. Clean credit usage, documented income, and organized assets tend to move smoothly through the system. Irregularities, even small ones, can trigger deeper scrutiny.

For a first-time buyer or investor, debunking AUS changes your approach. You’re no longer guessing what a lender wants—you’re preparing way ahead in advance positioning your financial profile to impress such a system designed to measure risk at scale.

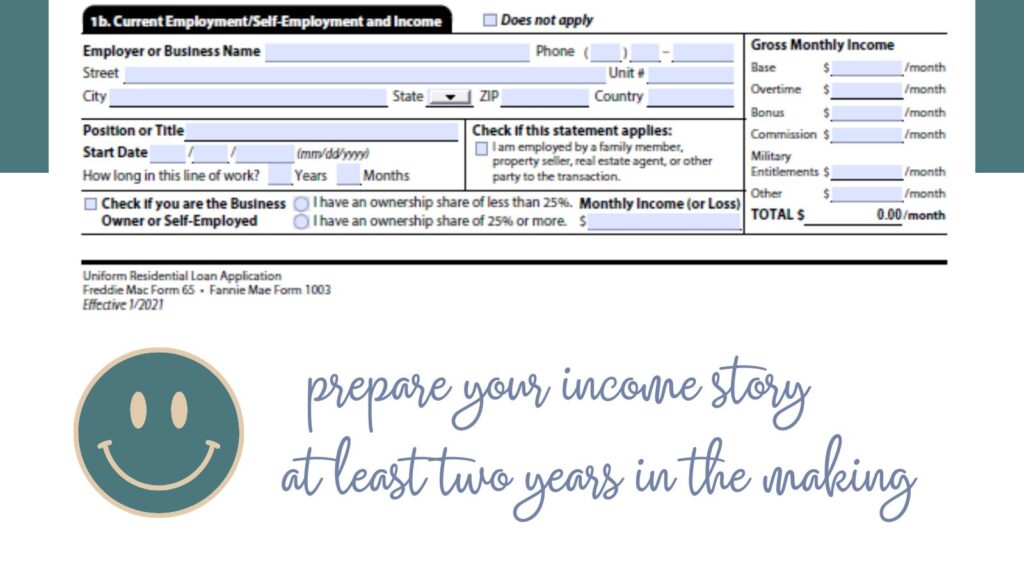

3. Employment and Income

This section tells your income story. You’ll include the following:

- Employer name and contact info

- Job title and length of employment

- Base income (salary or hourly)

- Additional income (bonus, commission, rental, etc.)

If your are self-employed:

You would have to provide business details and likely additional supporting documentation. It’s also important to include any part-time income, side gigs, or any form of bank deposits. But most importantly, it must be verifiable, stable, and likely to continue.

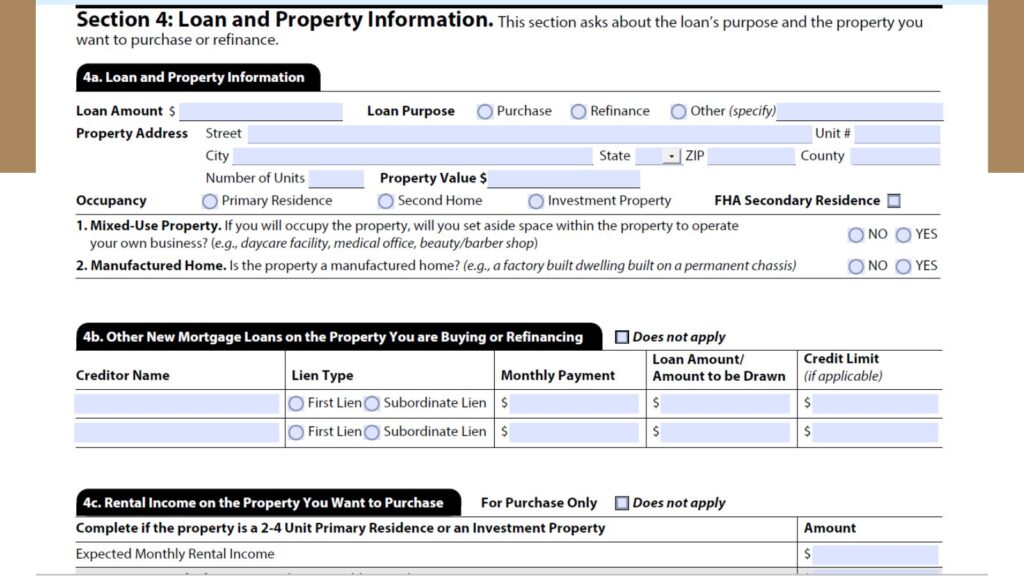

4. Loan and Property information

You’ll specify:

- Loan amount requested

- Property address that you are purchasing (if you haven’t identified the property yet, especially if you are a first time buyer, you may leave this blank)

- Loan purpose (purchase, refinance, construction)

- What is the Occupancy type, are you going to live there.

- Primary residence

- Second home

- Investment property

All your answers directly affect loan structure and pricing. So make sure if you have any questions. Call or email me directly if you have any questions.

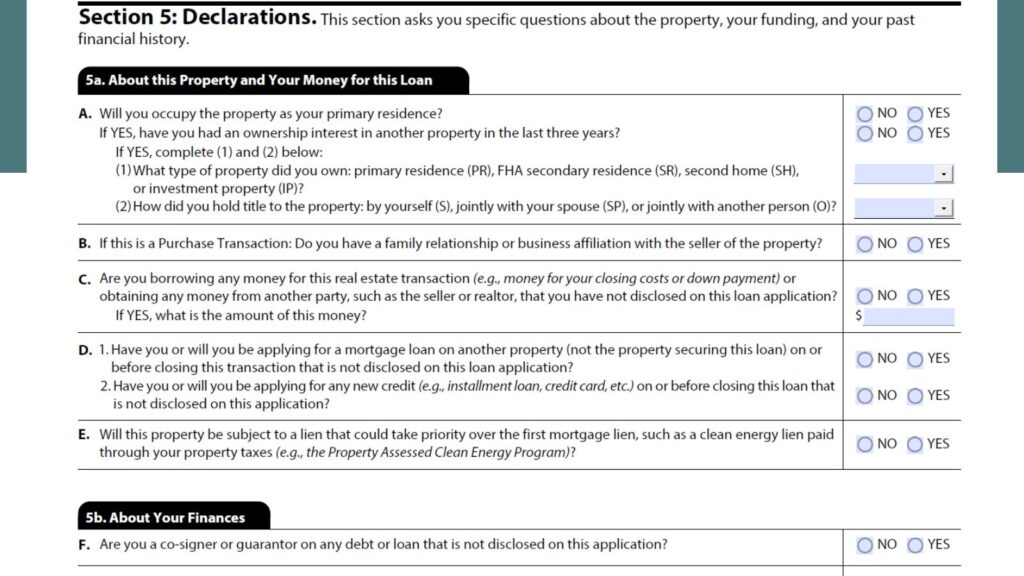

5. Declarations

This is a series of yes/no questions about your financial and legal background.

- Do you have any bankruptcy history

- Foreclosures or short sales

- Lawsuits or judgments

- Delinquent federal debt

- Ownership in other properties

Be honest. Always. Inconsistencies here can stop a loan—even late in the process.

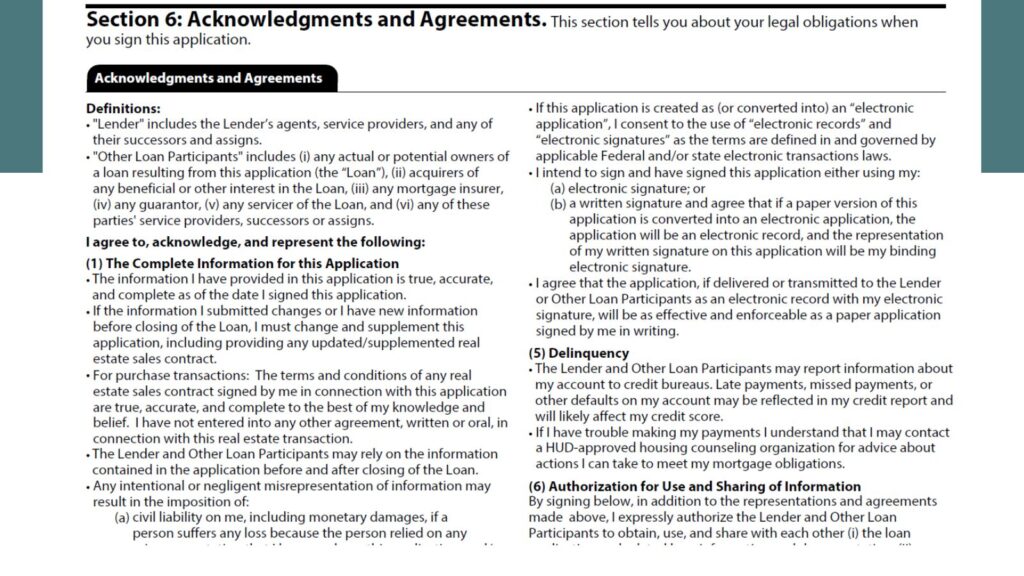

6. Acknowledgments and Agreements

This next section outlines the borrower’s legal acknowledgements and agreements. By signing this section, you confirm that the information provided is true and complete, authorize the lender to verify your financial information. It’s an important section that establishes your legal responsibilities throughout the loan process. This is where you:

- Confirm the information is accurate

- Authorize the lender to verify your data

- Agree to credit checks

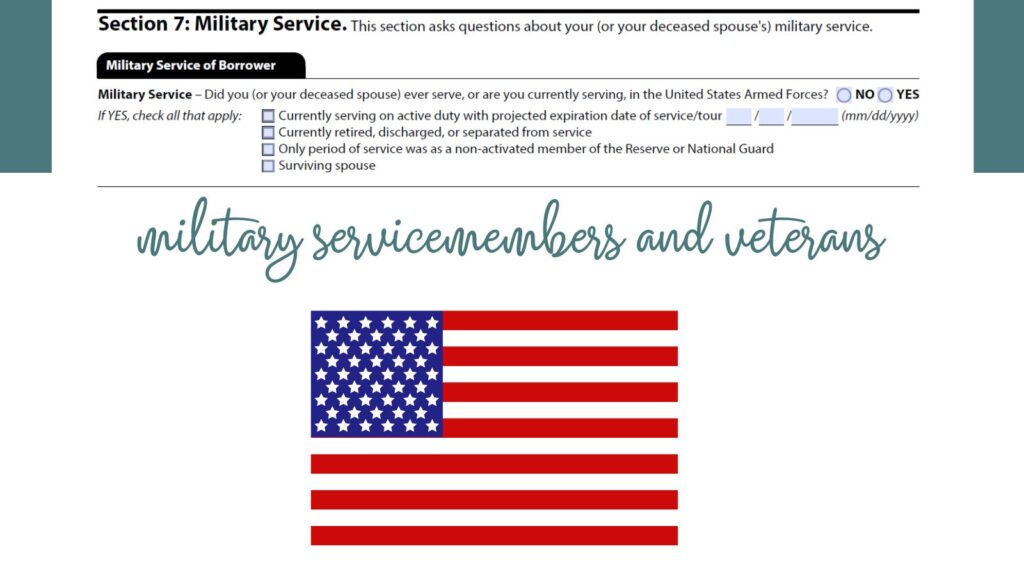

7. Military Service

This section gathers information about your military service, including whether you are currently serving, a veteran, or an eligible surviving spouse. Check off what applies to you and if you’re currently on active duty to include the projected expiration date of service tour.

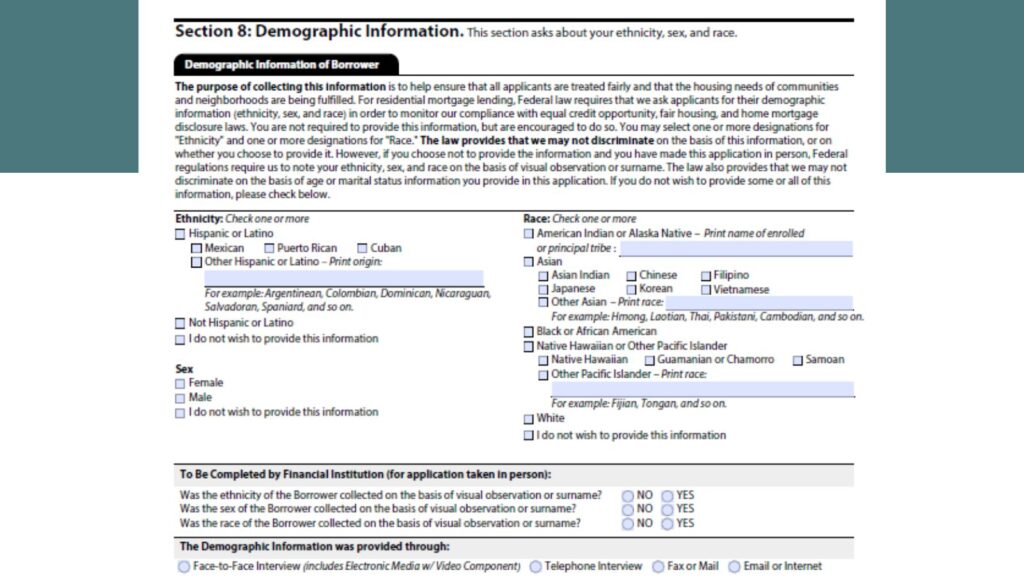

8. Demographic information (optional)

This section asks about:

- Race

- Ethnicity

- Gender

This section in Form 1003 is optional and used for regulatory and fair lending purposes. Skipping this part, does not impact your loan approval. But I recommend to fill it out anyway. It’s better to complete this form in its entirety because you want it to look good and complete. It’s like an essay of your life, fill-in the blank form. Impress for success!

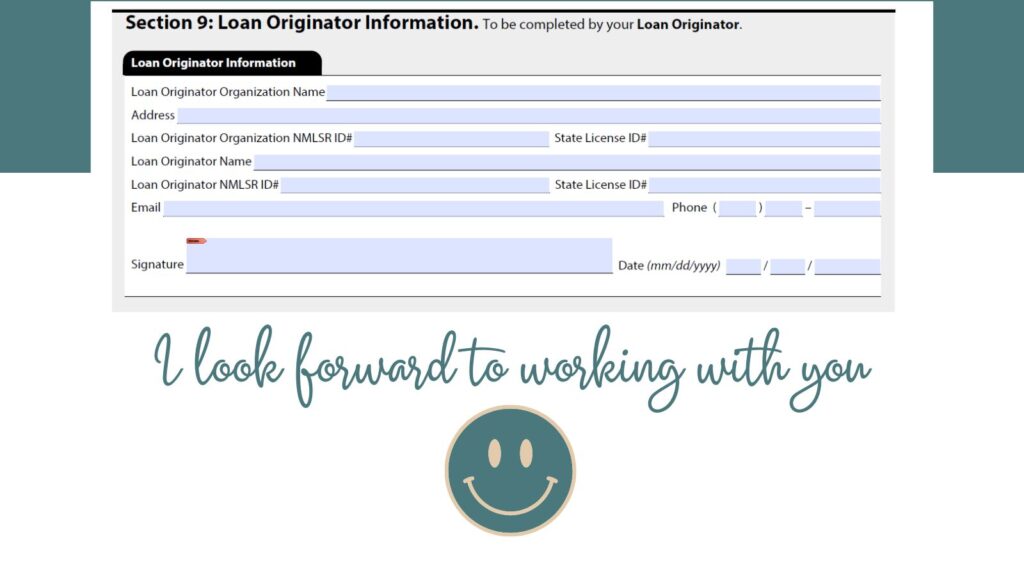

9. Loan Originator information

If I’m your mortgage loan originator, I will put my information in this section.

- My Name

- NMLS ID

- and my Broker and Company info

This ensures transparency and accountability in the transaction.

This is pretty much the entire form, for some of you, filling it out might take minutes, hours, days or even months. If this form has been sitting on your desk for a few months now—It’s time to make the call. Schedule an appointment with me to disable your procrastination 🙂

I’d like to commend you for taking the first small step into your new mindset of Ownership. Creating your first application to accomplish your goal of real estate property ownership.

If you would like to know what your current income could qualify for and would like to get more information or to find out an alternative approach to home affordability, please contact me by setting up a free consultation.

Let’s be friends on social media, like, subscribe, follow and say hello.